Managing Rent Receivables: Concepts, Accounting, and Financial Impact

Subsequent lease accounting under ASC 842 also requires any prepaid amounts to be recorded to the ROU asset. The debit for this journal entry will be to rent expense, increasing expense on the income statement. This represents the benefit received in the period from the occupation or use of the leased asset.

Accrued rent vs deferred rent

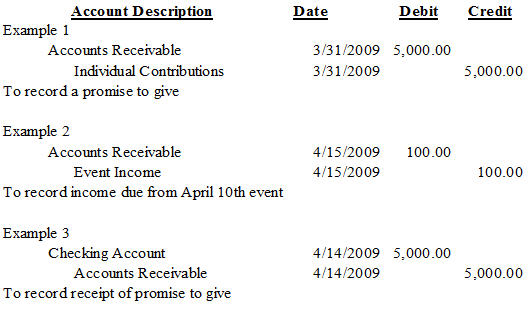

For any lease commencing after transition to ASC 842, deferred rent is not recognized. Instead, the difference between the straight-line rent expense and the cash paid is reflected in the net activity in the lease liability and ROU asset accounts each month. According to accrual accounting principles, rent receivable should be recognized when it is earned, regardless of when the payment is actually received. This means that if a tenant occupies a property in a given month, the rent for that month should be recorded as receivable at the end of the period, even if the payment is not due until the following month. This approach ensures that financial statements reflect the true economic activity of the period. It is important to note the difference between rent receivable and rent revenue accounts when recording transactions in the accounting records.

Rent Receivables and Cash Flow

This article explores rent expense and the impact of the adoption of ASC 842. It provides insights into the recognition and presentation of rent expense in financial statements, complete with an example at the end of the article to illustrate rent expense measurement. Rent Receivable is an asset account in the general ledger of a landlord which reports the amount of rent that has been earned but not received as of the date of the balance sheet. Any Leased shop requires a non-refundable security deposit of $100,000 with a minimum lease term of 2 years. An advance amount of $30,000 is to be paid just after entering into the Lease agreement.

Capital/Finance Lease vs. Operating Lease Explained: Differences, Accounting, & More

The management of rent receivables significantly influences a company’s financial statements, particularly the balance sheet and income statement. When rent receivables are accurately recorded, they appear as current assets on the balance sheet, enhancing the company’s asset base. This increase in assets can improve the company’s liquidity ratios, such as the current ratio, which measures the ability to cover short-term liabilities with short-term assets. A higher current ratio can be a positive indicator to investors and creditors, suggesting that the company is in a strong position to meet its obligations. The recognition of rent receivables must adhere to the accrual basis of accounting, where revenue is recorded when earned, not necessarily when received. This principle ensures that financial statements reflect the true financial position of the business.

- AI-driven chatbots can handle routine tenant inquiries about rent payments, freeing up human resources for more complex tasks.

- When the actual rent amount is paid, any variance from the minimum threshold used in the initial valuation is recorded directly to rent or lease expense.

- Instead accrued rent will now be reflected in the balance sheet as an adjustment to the newly capitalized ROU asset.

- For example, let’s examine a lease agreement that includes a variable rent portion of a percentage of sales over an annual minimum.

- Along with recognizing the asset and liability, the lessee also pays $10,000 of IDC which is recorded as an increase to the ROU asset.

- When rent is paid in advance of its due date, prepaid rent is recorded at the time of payment as a credit to cash/accounts payable and a debit to prepaid rent.

By leveraging data analytics tools, property managers can forecast tenant payment behaviors and identify patterns that may indicate future delinquencies. This proactive approach allows for early intervention, such as personalized payment plans or targeted communication strategies, to address potential issues before they become problematic. In addition to recording receivables, it’s important to account for potential bad debts. This allowance is an estimate of the receivables that may not be collected and is recorded as a contra-asset account, reducing the total receivables on the balance sheet. This practice aligns with the conservatism principle in accounting, ensuring that assets are not overstated.

Prepaid Rent and Other Rent Accounting for ASC 842 Explained (Base, Accrued, Contingent, and Deferred)

Organizations may have a commercial leasing arrangement or a rental agreement. Under ASC 842, accrued rent is no longer recognized as its own line item on the financial statements. The ROU asset is calculated as the lease liability, which is derived from the present value of future cash payments, adjusted for some specific reconciling items, including prepaid, accrued, and deferred rent. The excess expense recorded over the total cash paid has been accrued or deferred until the cash payments are larger than the expense recognized and the accumulated liability is depleted to zero.

The act of recognizing the expense when the company is obligated to pay for the use of the asset but before payment is made is called accruing the expense. Whenever the rent is rent receivable journal entry paid, the accrued rent will be reduced by the amount paid. What changed upon transition to ASC 842 is the requirement that lessees record operating leases on the balance sheet.

Also, tenants who have rented the property or office premises have to deduct TDS on the rent amount payable to the landlord. Step 2 – Transferring receipt of rental income to the income statement (profit and loss account). The Rent Receivable account is important in tracking the amount of money that has been earned but not yet collected from tenants.

When the periodic payments are structured so they can not be calculated without the occurrence of an event, such as a number of sales or units produced, the payments are not considered fixed rent. Let’s assume this is an operating lease, and the retailer transitioned to ASC 842 on January 1, 2022 and utilized a 7% borrowing rate for the present value calculation. Rent Payable is a liability account in the general ledger of the tenant which reports the amount of rent owed as the date of the balance sheet. It is shown on the credit side of an income statement (profit and loss account).

Leave a Reply

Want to join the discussion?Feel free to contribute!