Current Ratio Definition, Explanation, Formula, Example and Interpretation

The current ratio is one tool you can use to analyze a company and its financial state. An interested investor might also want to look at other key considerations like an organization’s profit margins and quick ratio, for example. Another factor that may influence what constitutes a “good” current ratio is who is asking. These are future expenses that have been paid in advance that haven’t yet been used up or expired. Generally, prepaid expenses that will be used up within one year are initially reported on the balance sheet as a current asset.

© Accounting Professor 2023. All rights reserved

Often, the current ratio tends to also be a useful proxy for how efficient the company is at working capital management. In actual practice, the current ratio tends to vary by the type and nature of the business. Everything is relative in the financial world, and there are no absolute norms. If a company has a current ratio of 100% or above, this means that it has positive working capital.

What Are Some Common Reasons for a Decrease in a Company’s Current Ratio?

However, this may not always be the case, and inaccurate asset valuation can lead to misleading current ratio results. For example, let’s say that Company F is looking to obtain a loan from a bank. The bank may evaluate Company F’s current ratio to determine its ability to repay the loan.

- This approach is considered more conservative than other similar measures like the current ratio and the quick ratio.

- The offers that appear on this site are from companies that compensate us.

- For example, if a company’s current assets are $80,000 and its current liabilities are $64,000, its current ratio is 125%.

- Analysts must also consider the quality of a company’s other assets versus its obligations as well.

- For every $1 of current debt, COST had $.98 cents available to pay for the debt at the time this snapshot was taken.

Free Course: Understanding Financial Statements

The ideal current ratio can vary by industry, and investors must consider industry-specific variations when evaluating a company’s current ratio. For example, retail businesses may have a higher current ratio due to the nature of their inventory turnover. It is important to note that the optimal current ratio can vary depending on the company’s industry.

As the amount expires, the current asset is reduced and the amount of the reduction is reported as an expense on the income statement. Learn how to build, read, and use financial statements for your business so you can make more informed decisions. Various factors, such as changes in a company’s operations or economic conditions, can influence it. Monitoring how to design products with operations management in mind a company’s Current Ratio over time helps in assessing its financial trajectory. For instance, if a company’s Current Ratio was 2 last year but is 1.5 this year, it may suggest that its liquidity has slightly decreased, which could be a cause for further investigation. For the last step, we’ll divide the current assets by the current liabilities.

What Is a Good Current Ratio for a Company to Have?

One of the simplest ways to improve a company’s current ratio is to increase its current assets. This can be achieved by increasing cash reserves, accelerating accounts receivable collections, or reducing inventory levels. By increasing its current assets, a company can improve its ability to meet short-term obligations.

High inventory levels can slow liquidity, making the quick ratio a valuable tool to focus on truly liquid assets. A quick ratio of 2.0 shows that your company has twice as many liquid assets as needed to cover its short-term liabilities. It’s ideal to use several metrics, such as the quick and current ratios, profit margins, and historical trends, to get a clear picture of a company’s status. Furthermore, a high current ratio can make it difficult for a company to generate a strong return on investment for shareholders. This is because excess cash and inventory do not generate returns like investments in new projects or debt repayments can. A high current ratio can signal that a company is not taking advantage of investment opportunities or paying off its debts promptly.

Many entities have varying trading activities throughout the year due to the nature of industry they belong. The current ratio of such entities significantly alters as the volume and frequency of their trade move up and down. In short, these entities exhibit different current ratio number in different parts of the year which puts both usability and reliability of the ratio in question. Current liabilities refers to the sum of all liabilities that are due in the next year. On the other hand, a current ratio greater than one can also be a sign that the company has too much unsold inventory or cash on hand. Apple technically did not have enough current assets on hand to pay all of its short-term bills.

The current ratio is an important measure of liquidity because short-term liabilities are due within the next year. In this example, Company A has much more inventory than Company B, which will be harder to turn into cash in the short-term. Perhaps this inventory is overstocked or unwanted, which may eventually reduce its value on the balance sheet. Company B has more cash, which is the most liquid asset and more accounts receivable which could be collected more quickly than inventory can be liquidated.

Therefore, it is essential to consider the industry in which a company operates when evaluating its current ratio. There’s another common ratio used to look at a company’s liquidity — the quick ratio. Unlike the current ratio, which considers all current assets and liabilities, the quick ratio only looks at the most liquid assets (although it does include accounts receivable) versus the current liabilities. The current ratio helps investors and creditors understand the liquidity of a company and how easily that company will be able to pay off its current liabilities.

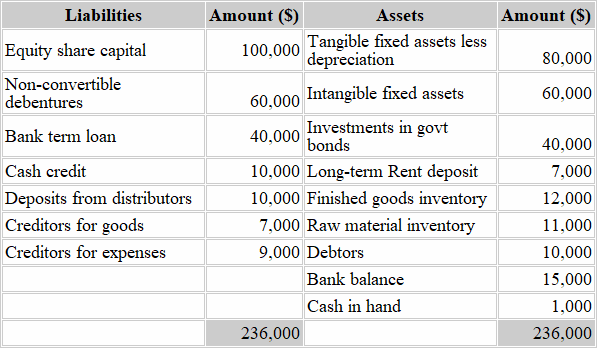

Current assets listed on a company’s balance sheet include cash, accounts receivable, inventory and other assets that are expected to be liquidated or turned into cash in less than one year. Current liabilities include accounts payable, wages, taxes payable, and the current portion of long-term debt. A current ratio of 1.5 would indicate that the company has $1.50 of current assets for every $1 of current liabilities. For example, suppose a company’s current assets consist of $50,000 in cash plus $100,000 in accounts receivable. Its current liabilities, meanwhile, consist of $100,000 in accounts payable. In this scenario, the company would have a current ratio of 1.5, calculated by dividing its current assets ($150,000) by its current liabilities ($100,000).

Leave a Reply

Want to join the discussion?Feel free to contribute!