Cash Book: Meaning, Types, and Example

For example, if cash is paid early, creditors may receive a discount. On the other hand, if debtors pay early, a discount may be allowed to them. At the end of fixed period, the petty cashier submits the details of petty expenses, and the chief cashier again advances a fixed amount for the next fixed period. If they record petty expenses in the main cash book, then both the chief cashier and the main cash book will be overburdened. The difference between the sum of the debit items and the sum of the credit items represents the balance of the petty cash in hand. Utility companies typically have high capital requirements, meaning free cash flow may be low or inconsistent due to ongoing reinvestment needs.

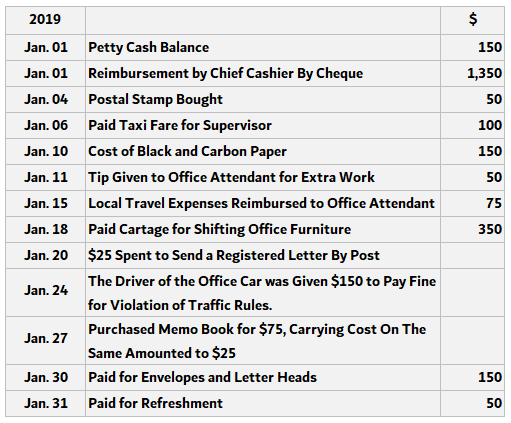

Petty Cash Book Template

Residual income valuation can capture the economic profit generated after meeting equity costs without relying solely on cash flows. By focusing on book value and earnings, the model helps analysts assess whether the utility’s investments are generating returns above the required rate, even in the face of heavy capital spending. The first line of each entry shows date, name of customer (if any), account to be debited (positive amount) or credited (negative amount). It also acts as a part of the ledger because it contains cash and bank accounts.

- Both the columns are totaled and balanced like a traditional T-account at the end of an appropriate period, which is usually one month.

- You could just buy a school exercise book which already has rows printed in it, so all you have to do is draw in the columns.

- The Total columns have formulas in them, so they update automatically.

- It will show the date of the transaction, name of the customer (if any), account to be debited (positive amount) or credited (negative amount).

How is Sales Tax Calculated

Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. A bank account may have an overdrawn balance because by arranging an overdraft with the bank, it is possible that more money may be withdrawn from the bank than what was deposited. It is worth mentioning that the format of a three column cash book is similar to that of a two column cash book.

Operation of Petty Cash

The two column cash book uses two columns on each side of the book. Depending on the nature of the business involved the two columns can be used for different purposes. The other side of the cash book has the heading ‘Credit’ and shows an identical format with the single column representing the monetary amount of the cash payment. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. If the debit column is larger than the credit column, the difference represents cash at bank. If, on the other hand, the credit column exceeds the debit column, the difference represents “overdrawn balance”.

The purpose/function of each column is briefly described in this section. Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping. He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own.

Submit to get your question answered.

It is also much faster to access cash information in a cash book than by following the cash through a ledger. A cash book is a separate ledger in which cash transactions are recorded, whereas a cash account is an account within a general ledger. A cash book serves the purpose of both the journal and ledger, whereas a cash account is structured like a ledger. Details or narration about the source or use of funds are required in a cash book but not in a cash account.

A cash book is a comprehensive record of cash transactions, including receipts, payments, bank deposits, and withdrawals. It records the transactions of both bank account and cash accounts. In order for a cash book to be accurate and up-to-date, it is important to record all transactions as soon as they happen. If money is received on Monday, but not recorded until Wednesday, the cash book will be inaccurate. A double-column cash book includes separate columns for recording receipts and payments, while a single-column cash book combines both types of transactions into one column.

When entries from the cash book are posted to ledger accounts, the relevant account number is written in this column. All the cash receipts are entered on the debit side, and cash payments are entered on the credit side. For simplicity, the single cash ledger book diagram below shows only one side of the cashbook, in this case the left hand, receipts side (debit).

However, two types of cash books are now commonly used for an organization’s aggregate demand. Here is what a simple profit and loss report would look like based on these cash book entries. Whiting out errors and writing over them makes it very difficult for anyone to be 100% sure that you have processed the accounts in good order (such as auditors).

The left shows income for cash and bank, and the right shows expenditures for both. The year, month, and day of the receipts and payments of cash are written in the date column on the debit and credit accessories sides of the cash book. In essence, a single column cash book is nothing but a cash account. A cash account cannot show a credit balance on the principle that you cannot pay what you do not have.